Fed Decision Preview: How Do US Interest Rates Affect the Stablecoin Industry?

Author: 0xYYcn Yiran (Bitfox Research)

The stablecoin market continues to surge in size and importance, driven by the popularity of the cryptocurrency market and the expansion of mainstream application scenarios. By mid-2025, its total market capitalization has exceeded $250 billion, an increase of more than 22% from the beginning of the year. According to a Morgan Stanley report, these dollar-pegged tokens currently have an average daily trading volume of over $100 billion and will drive on-chain transactions totaling $27.6 trillion in 2024. According to Nasdaq data, the transaction has surpassed Visa and Mastercard combined. However, behind this boom lies a series of hidden dangers, most notably the issuer's business model and the stability of its tokens are closely tied to changes in U.S. interest rates. As the next FOMC decision approaches, this study focuses on fiat-collateralized USD stablecoins (e.g., USDT, USDC), taking a global perspective and delving into how the Fed's interest rate cycle, along with other potential risks, will reshape the industry landscape.

Stablecoin 101: Growing in the Boom and Regulation

Stablecoin definition:

Stablecoins are crypto assets designed to maintain a constant value, with each token typically pegged to the US dollar at a 1:1 ratio. Its value stabilization mechanism is mainly achieved through two methods: backed by sufficient reserve assets (such as cash and short-term securities), or by relying on specific algorithms to regulate the supply of tokens. Fiat-collateralized stablecoins, such as Tether (USDT) and Circle (USDC), provide full collateral guarantees for each unit of token they issue by holding cash and short-term securities. This safeguard mechanism is at the heart of its price stability. According to the Atlantic Council, about 99% of stablecoin circulation is currently dominated by the dollar-denominated type

Industry significance and current situation:

In 2025, stablecoins are leaping out of the crypto space and accelerating their integration into mainstream financial and business scenarios. International payment giant Visa has launched a platform that supports banks in issuing stablecoins, Stripe has integrated stablecoin payment functions, and Amazon and Walmart are also planning to issue their own stablecoins. At the same time, global regulatory frameworks are taking shape. In June 2025, the U.S. Senate passed the landmark "Stablecoin Payment Clarity Act" (GENIUS Act), becoming the first stablecoin regulatory law at the federal level. Its core requirements include: issuers must maintain a stable 1:1 support ratio with high-quality liquid assets (cash or short-term Treasury bonds maturing within three months) and clarify the rights protection obligations of currency holders. In the transatlantic European market, the Markets in Crypto-Assets Regulation Act (MiCA) framework implements stricter regulations, giving authorities the power to restrict the circulation of non-euro stablecoins when stablecoins threaten the stability of eurozone currencies. At the market level, stablecoins have shown strong growth momentum: as of June 2025, their circulating value has exceeded $255 billion. Citi predicts that the market size is expected to surge to $1.6 trillion by 2030, a growth of about seven times. This clearly shows that stablecoins are becoming mainstream, but their rapid growth also brings new risks and frictions.

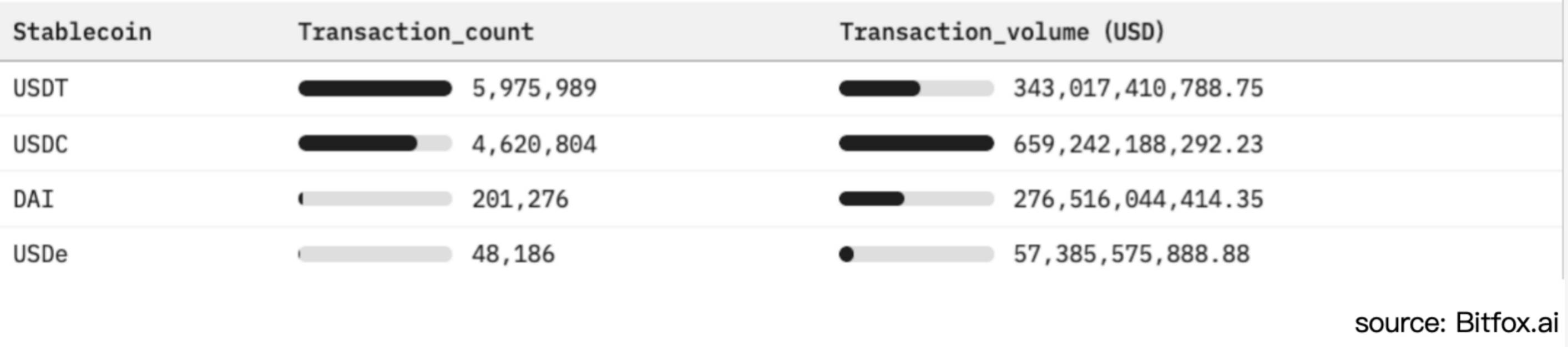

Figure 1: Ethereum stablecoin adoption comparison and market activity analysis (last 30 days)

Fiat currency supports stablecoins and interest rate-sensitive models

Unlike traditional bank deposits, which generate interest on customers, stablecoin holders typically do not enjoy any income. According to the GENIUS Act, the user account balance of fiat-collateralized USD stablecoins is clearly set to interest-free (0%). This regulatory arrangement allows issuers to retain all the proceeds generated from their reserve investments. In the current environment of high interest rates, this mechanism has enabled companies such as Tether and Circle (USD Coin issuer) to become highly profitable entities. However, this model also exposes it to a high degree of vulnerability in downward interest rate cycles

Reserve Investment Structure:

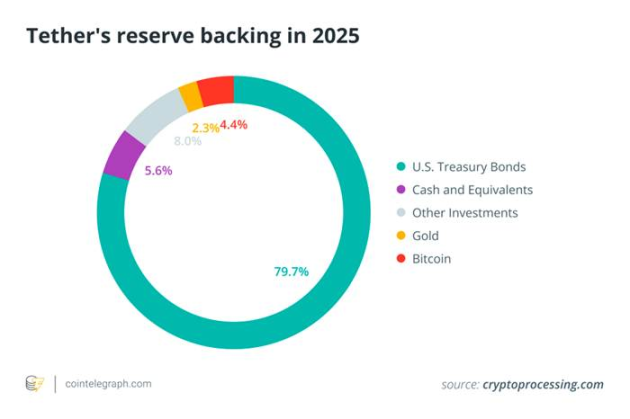

To ensure liquidity and maintain the value of stablecoins, major issuers allocate the bulk of their reserves to short-term U.S. Treasury bonds (U.S. Treasury bonds). Treasury bills) and other short-term financial instruments. As of early 2025, Tether holds $113 billion to $120 billion in U.S. government debt, accounting for about 80% of its total reserves, ranking among the top 20 U.S. Treasury holders in the world. The chart below shows the detailed composition of Tether's reserve asset allocation, clearly showing that its assets are highly concentrated in Treasury bonds and cash assets, with other securities, gold, and non-traditional assets such as Bitcoin accounting for a significantly lower proportion of the portfolio

Figure 2. The composition of Tether's reserve assets in 2025 (dominated by U.S. Treasury bills) reflects the high reliance of fiat-backed stablecoins on interest-bearing government assets

High-quality reserve assets maintain their pegged value and enhance user confidence while also generating substantial interest income – the lifeblood of the current stablecoin business model. Between 2022 and 2023, the Federal Reserve's aggressive interest rate hikes pushed short-term Treasury yields (T-bills) and bank deposit rates to multi-year highs, directly amplifying the investment returns of stablecoin reserves. Taking Circle's financial report as an example, of its total revenue of $1.68 billion in 2024, up to $1.67 billion (accounting for 99%) comes from interest income from reserve assets. On the other hand, according to Techxplore, Tether's corporate profit in 2024 is reported to be $13 billion, which is enough to match or surpass the profitability of leading Wall Street banks such as Goldman Sachs. This scale of profitability (created by Tether's operating team of about 100 people) particularly highlights the strong boost effect of a high-interest rate environment on stablecoin issuers' revenues. Essentially, stablecoin issuers operate a high-return "carry trade," where user funds are allocated to treasury bond assets with yields exceeding 5% and receive the full yield of the spread because users accept zero interest rates. Vulnerability to interest rate fluctuations.

Interest rate fluctuation risk exposure

Stablecoin issuers' revenue models are highly sensitive to changes in the Fed's interest rates. For example, a rate cut of just 50 basis points (0.50%) could lead to a sharp decline in Tether's annual interest income by about $600 million. As Nasdaq analysts warned, "Overreliance on interest income will leave issuers like Circle vulnerable in the rate cut cycle." ”

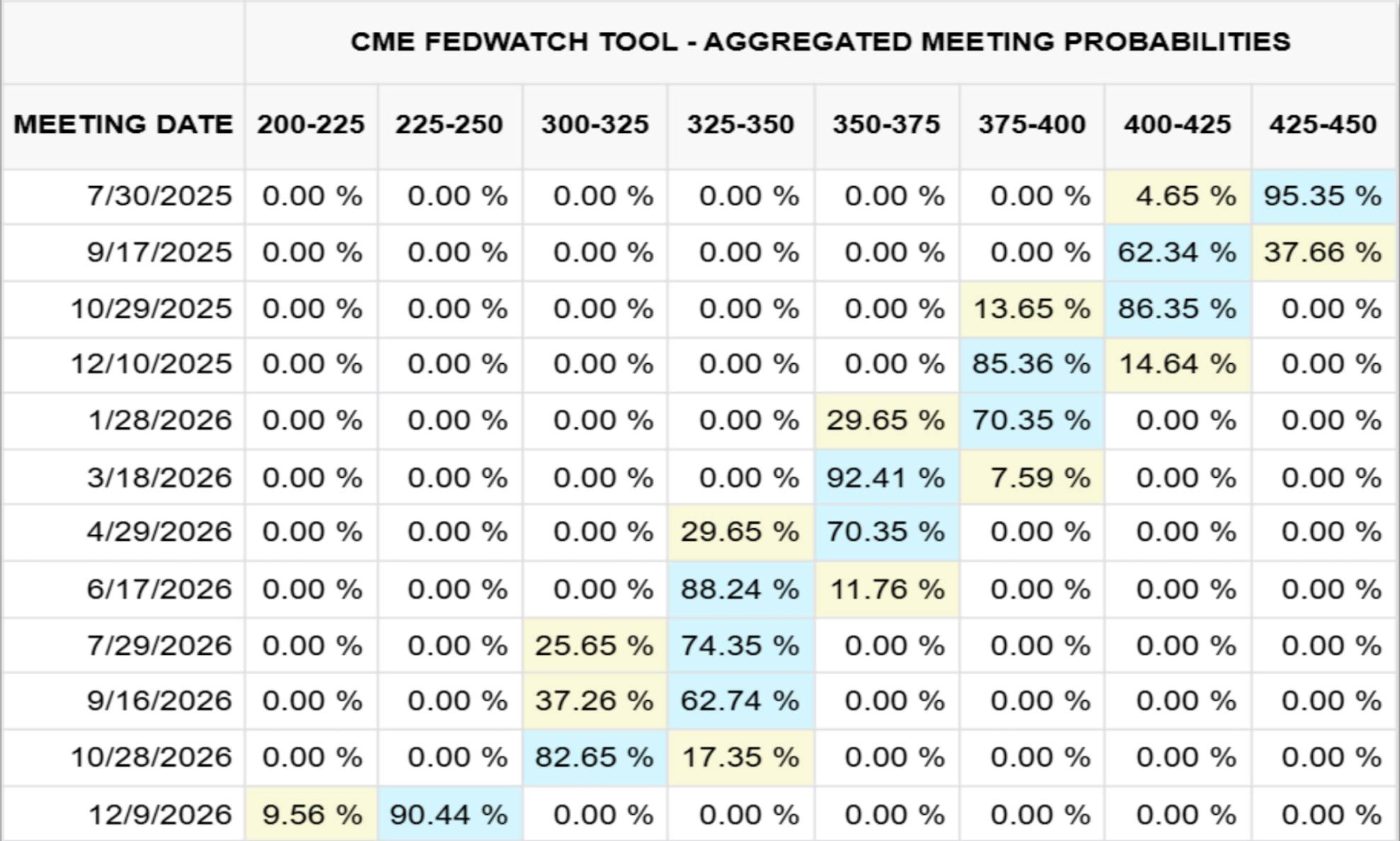

Figure 3 below shows the direction of the federal funds rate curve plotted by the Chicago Mercantile Exchange (CME) based on market expectations on July 23, 2025 (forecast period to the end of 2026); Figure 4 illustrates the impact mechanism of interest rate changes on Circle's reserve income through quantitative analysis on the order of millions of dollars.

Figure 3. December 2026 Fed Funds Rate Outlook (CME, 2025/07/23)

Figure 4. Sensitivity of Circle reserve income to changes in interest rates

In 2024, for example, Circle's interest income on reserve assets reached $1.67 billion, accounting for 99% of its total revenue ($1.68 billion). Based on the Chicago Mercantile Exchange (CME) data model (as of July 23, 2025), if the federal funds rate falls back to the 2.25%–2.50% range in December 2026 (with a probability of about 90%), Circle expects to lose approximately $882 million in interest income, more than 50% of its total related income in 2024. To cover this revenue gap, the company must double the circulating supply of its USDC stablecoin by the end of 2026.

Other core risks besides interest rates: multiple challenges of the stablecoin system

While interest rate dynamics hold a central position in the stablecoin industry, there are several other key risks and challenges within the system. In the context of industry optimism, there is an urgent need to systematically summarize these risk factors to provide a calm and comprehensive analysis:

Regulatory and legal uncertainty

Stablecoin operations are now subject to fragmented regulatory frameworks such as the GENIUS Act in the United States and the Markets in Crypto-Assets Regulation Act (MiCA) in the European Union. While the framework gives legitimacy to some issuers, it also brings high compliance costs and sudden market access restrictions. Enforcement actions by regulators against insufficient transparency of reserves, circumvention of sanctions (such as Tether's multi-billion dollar transactions in sanctioned territories), or infringement of consumer rights can quickly lead to the suspension of the redemption function of certain stablecoins or their removal from the core market.

banking cooperation and liquidity concentration risk

The reserve custody and fiat channel (deposit/withdrawal) services of fiat-collateralized stablecoins are highly dependent on limited cooperative banks. Sudden crises at cooperative banks (such as the collapse of SVB at Silicon Valley Bank that froze $3.3 billion worth of USDC reserves) or large-scale waves of centralized redemptions can quickly deplete bank deposit reserves, trigger token decoupling, and threaten the liquidity stability of the broader banking system when wholesale redemption pressure breaks through bank cash buffers.

Anchoring stability and deanchoring risk

Even if fully collateralized, stablecoins can and do have collapsed when market confidence falters (e.g., USDC plummeted to $0.88 in March 2023 due to concerns about accessibility of reserve assets). Algorithmic stablecoins have a steeper robustness curve, as evidenced by the collapse of TerraUSD (UST) in 2022.

Transparency and counterparty risk

Users rely on Attestations published by issuers (usually quarterly) to assess asset authenticity and liquidity. However, the lack of a comprehensive public audit raises doubts about its credibility. Whether it is cash deposited with banks, money market fund shares or repurchase agreement assets, reserve assets contain counterparty risk and credit risk, which can substantially damage the ability to redeem guarantees under stressful scenarios.

Operational and technical security risks

Centralized stablecoins can freeze or confiscate tokens in response to attacks, but they also pose a single point of governance risk. DeFi versions are vulnerable to smart contract vulnerabilities, cross-chain bridge attacks, and hacking of custodians. At the same time, factors such as user errors, phishing, and irreversible blockchain transactions also pose daily security challenges to coin holders.

Hidden dangers of macro financial stability

Hundreds of billions of dollars in stablecoin reserves are concentrated in the short-term U.S. Treasury market, and their large-scale redemptions will directly affect the demand structure and yield volatility of Treasury bonds. Extreme outflow scenarios may trigger fire-sales in the Treasury market; The widespread use of stablecoins in dollarization may weaken the transmission of the Federal Reserve's (Fed) monetary policy, thereby accelerating the development of US central bank digital currencies (CBDCs) or the establishment of stricter regulatory guardrails.

conclusion

As the next FOMC meeting approaches, while the market generally expects interest rates to remain unchanged, the next meeting minutes and forward guidance will be in focus. The significant growth of fiat-collateralized stablecoins such as USDT and USDC masks the nature of their business model that is deeply tied to changes in U.S. interest rates. Looking ahead, even modest rate cuts (e.g., 25-50 basis points) could erode hundreds of millions of dollars in interest income, forcing issuers to reassess their growth path or maintain market adoption by transferring a portion of the proceeds to holders.

In addition to interest rate sensitivity, stablecoins must navigate the evolving regulatory environment, banking and liquidity concentration risks, anchoring integrity challenges, and operational risks ranging from smart contract vulnerabilities to insufficient reserve transparency. Crucially, when such tokens become systemically important holders of short-term U.S. Treasury bonds, their redemption behavior may impact the pricing mechanism of the global bond market and interfere with the transmission path of monetary policy effectiveness.